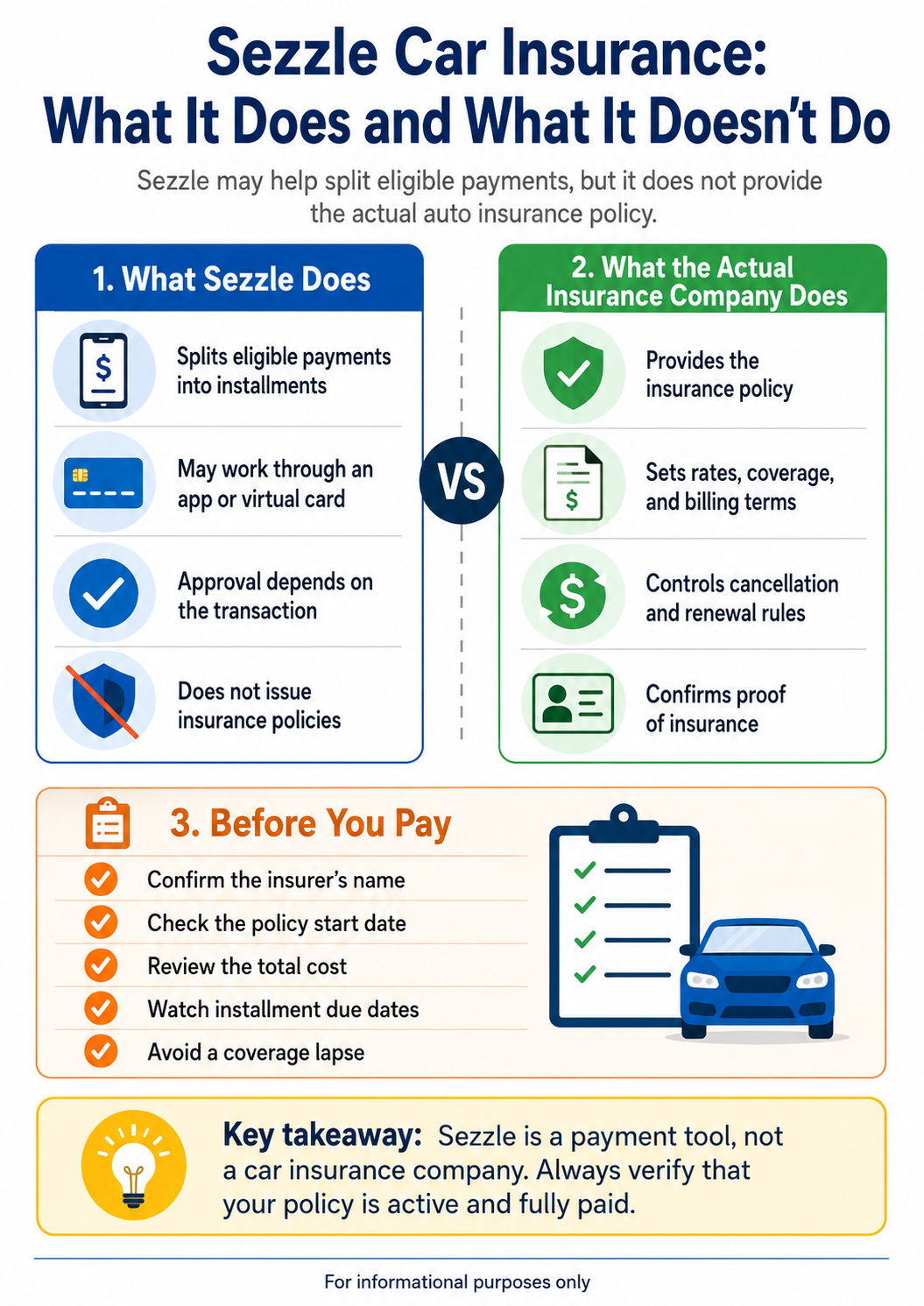

Sezzle car insurance is a phrase many drivers search when they want coverage without a large upfront payment. The important detail is that Sezzle is not an auto insurance company, does not underwrite policies, and does not decide whether you qualify for coverage. It is a buy now, pay later payment platform that may help split certain eligible purchases into installments.

That difference matters. Paying with Sezzle, a virtual card, or another BNPL-style method does not replace the need to choose a real insurer, confirm your policy start date, read the billing terms, and keep every payment current. If your goal is simply to lower the amount due today, you should compare Sezzle-style payment flexibility against direct insurer installment plans, no upfront payment car insurance, and broader pay later solutions.

Quick answer: You may be able to use Sezzle in some insurance-related payment flows, especially where a virtual card or eligible checkout option is accepted. However, the safest approach is to verify the actual insurance company, down payment, installment schedule, cancellation rules, fees, and proof-of-insurance timing before relying on any BNPL payment method.

How Sezzle Works for Car Insurance Payments

Sezzle’s general buy now, pay later model is built around splitting purchases into smaller payments over time. Sezzle’s own materials describe Pay in 4 installment options, and its car insurance page discusses using Sezzle for car insurance-related purchases through the app and a virtual card process. That can sound simple, but auto insurance billing is more complicated than buying a normal retail item.

With car insurance, the payment method is only one part of the transaction. The insurer or agency still controls the policy terms, underwriting decision, effective date, required down payment, renewal rules, cancellation rules, and proof of insurance. A BNPL approval does not mean the insurance policy itself has been approved, and an insurance quote does not guarantee that every payment method will be accepted.

In practical terms, Sezzle may be relevant if the checkout flow accepts it directly, if the Sezzle app routes you to an eligible payment option, or if a virtual card can be used where the insurer or agency accepts card payments. Even then, the driver should confirm that the payment successfully posts to the insurance account and that coverage is active before driving.

Sezzle Is Not the Same as No-Deposit Car Insurance

One reason the phrase “Sezzle car insurance” can be confusing is that shoppers often use it as a shortcut for “I need car insurance now but cannot pay a large amount today.” Those are related ideas, but they are not identical.

No-deposit car insurance usually refers to policies marketed with a lower first payment or reduced upfront cost. A direct insurer installment plan is a billing arrangement attached to the insurance policy. Sezzle, by contrast, is a separate payment platform that may or may not work with the transaction you are trying to complete.

Sezzle or BNPL

A third-party payment option that may split an eligible transaction into installments. It does not create the insurance policy.

Insurer Installment Plan

A payment schedule offered by the insurer or agency. This is usually tied directly to the policy billing system.

No-Deposit Option

A marketing term often used for policies with a smaller first payment. The total cost may still be spread over the policy term.

When Sezzle Might Make Sense

Sezzle may be worth considering when you have already compared real auto insurance quotes and simply need a more flexible way to handle the payment. It may also make sense for drivers who are comfortable managing installment due dates and who have verified that the payment method is accepted for the exact transaction.

For example, a driver may want to avoid putting the full first payment on a high-interest credit card. Another driver may need a short-term budgeting bridge while waiting for a paycheck. In those situations, a BNPL tool can feel helpful. But the driver still needs to make sure the insurance account shows the premium as paid and that there is no delay in coverage activation.

Drivers who need proof of coverage quickly should also compare dedicated instant coverage options, because speed matters. A payment tool is not useful if the policy is not active when you need it.

When Sezzle May Be the Wrong Choice

Sezzle may be a poor fit if you are already struggling to keep up with other bills, if you are unsure whether the payment will be accepted by the insurance company, or if splitting the payment only delays a cost you cannot realistically afford. BNPL can make a payment look smaller, but it does not make the insurance policy cheaper by itself.

It can also create a timing problem. Your Sezzle installment due dates may not match your insurer’s billing schedule. If a later installment fails, that does not necessarily mean the insurer will wait. Insurance companies can cancel policies for nonpayment according to state rules and policy terms. That is why the safest choice is the one that keeps your coverage active, predictable, and affordable beyond the first payment.

Sezzle vs. Direct Monthly Car Insurance Payments

For many drivers, a direct monthly payment plan from the insurer may be simpler than using a third-party BNPL platform. Direct billing usually keeps the payment schedule, policy status, renewal notices, and cancellation notices inside one insurance account. Sezzle may add flexibility, but it also adds another system to monitor.

| Option | How it works | Main benefit | Main risk |

|---|---|---|---|

| Sezzle or BNPL | Splits an eligible payment into installments through a third-party platform or virtual card. | Can reduce immediate payment pressure if accepted. | May not be accepted by every insurer or may create separate due dates to manage. |

| Insurer monthly plan | The insurance company bills the premium over the policy term. | Usually easier to track because billing is tied directly to the policy. | May require a down payment, installment fees, or autopay enrollment. |

| Low down payment policy | The first payment is reduced, then the remaining premium is billed later. | Can help drivers start coverage with less due today. | Total premium may still be high, and missing payments can risk cancellation. |

| Credit card | The policy payment is charged to a card and repaid through the card issuer. | May be widely accepted and easy to process. | Interest can become expensive if the balance is not paid quickly. |

What to Check Before Using Sezzle for Insurance

Before using Sezzle or any BNPL method for an insurance-related payment, verify the full payment path. The goal is not just to make a payment go through. The goal is to keep your policy active without surprise fees, failed payments, or a coverage lapse.

Better Alternatives to Compare First

If your main concern is affordability, Sezzle should not be the only option you compare. In many cases, the better solution is finding an insurance company or agency that offers a lower first payment, monthly billing, autopay discounts, or a policy structure that fits your budget from the beginning.

- Start with no upfront payment car insurance if your biggest issue is the first payment.

- Review pay later car insurance contracts if you want to understand billing terms more clearly.

- Compare low monthly payment strategies if your budget problem is ongoing, not just upfront.

- Read about BNPL car insurance for first-time drivers if you are new to insurance shopping.

- Use our no credit check pay later insurance guide if approval concerns are part of the issue.

Practical Example: When the Payment Looks Easy but the Policy Still Matters

Imagine a driver finds a quote with a first payment due today. The driver opens Sezzle, creates a virtual card, and tries to use it during checkout. If the card is accepted and the insurer confirms the policy is active, the driver may have successfully reduced the immediate cash pressure.

But there are still follow-up responsibilities. The driver must make every Sezzle installment on time. The driver must also watch the insurance account to make sure the payment was posted correctly and that future insurer payments are scheduled. If the BNPL payment fails or the policy billing account shows unpaid premium, the driver could still face cancellation or a lapse.

That is why Sezzle should be treated as a payment method, not as an insurance solution by itself. The real solution is affordable coverage that stays active month after month.

Is Sezzle Car Insurance Legit?

The phrase is partly legitimate and partly misleading. It is legitimate in the sense that Sezzle publicly discusses using its platform for car insurance-related purchases. It is misleading if someone presents Sezzle as the company providing the auto insurance policy.

A safer way to think about it is this: Sezzle may help with the payment side of an eligible transaction, but your coverage still comes from the insurer. Before paying, confirm the carrier, coverage limits, deductibles, liability protection, policy period, cancellation terms, and renewal expectations.

Editorial recommendation: Do not choose an insurance option only because the first payment looks smaller. Choose the option that gives you real coverage, clear billing, a manageable total cost, and the lowest risk of cancellation.

FAQ About Sezzle Car Insurance

Does Sezzle sell car insurance?

No. Sezzle is a buy now, pay later payment platform. It does not underwrite auto insurance policies, set insurance rates, or act as your insurance carrier.

Can I use Sezzle to pay for car insurance?

Possibly, but it depends on the checkout flow, merchant, insurer, agency, virtual card acceptance, and Sezzle approval. Always confirm that the payment posts successfully and that your policy is active.

Is Sezzle better than monthly car insurance payments?

Not always. A direct monthly plan from the insurer may be easier to manage because the billing schedule is tied directly to the policy. Sezzle may help in some cases, but it creates a separate payment schedule to track.

Can using Sezzle prevent a car insurance lapse?

Only if the payment is accepted, posted correctly, and followed by all required future payments. A BNPL tool does not remove the risk of cancellation if premiums are not paid according to the policy terms.

What should I compare before using BNPL for insurance?

Compare the total premium, down payment, installment fees, due dates, payment method rules, cancellation notice terms, proof-of-insurance timing, and the financial strength of the actual insurer.

Final Verdict: Use Sezzle Carefully, Not Blindly

Sezzle can be part of the conversation for drivers who want more payment flexibility, but it should not be treated as a replacement for real insurance shopping. The best option is usually the one that combines affordable coverage, clear billing, reliable proof of insurance, and a payment schedule you can actually keep.

If Sezzle works for your transaction and does not add extra risk, it may help reduce upfront pressure. If it creates confusion, separate due dates, or uncertainty about whether the policy is active, a direct insurer installment plan or a low-down-payment policy may be safer.

Compare Pay Later Car Insurance Options

Before relying on Sezzle or any third-party payment app, compare real insurance options built around flexible billing, lower upfront costs, and clear policy terms.

Explore Pay Later Solutions