Last updated on April 8, 2026

The Buynowpaylatercarinsurance.com Editorial Team produces informational content about auto and home insurance topics, focusing on clear, practical explanations to help readers understand common coverage options and shopping considerations.

Articles cover everyday questions such as proof of insurance, minimum state requirements, pricing factors, and ways drivers may reduce costs while maintaining appropriate protection.

Content reviewed internally for clarity and consistency of general insurance concepts.

Note: This content is for general informational purposes only and does not constitute insurance, legal, or financial advice. Buynowpaylatercarinsurance.com is an independent informational website and is not affiliated with any insurer.

Many drivers search for first month free auto insurance because they need coverage fast but cannot afford a large upfront payment. At first glance, the idea sounds simple: start your policy today and worry about the first bill later. In reality, true “free month” auto insurance is uncommon, but there are several legitimate options that can get you close to the same result.

This guide explains what first month free auto insurance usually means, when these offers are real, what to watch out for, and which alternatives may work better if you need coverage now without a heavy upfront cost.

- True first month free auto insurance is rare.

- Most offers are really deferred billing, small activation payments, or split-payment plans.

- The best alternatives are often no upfront payment options or low upfront cost plans.

- You should always compare the total cost, not just the first bill.

What Does “First Month Free Auto Insurance” Actually Mean?

In most cases, first month free auto insurance does not mean the insurer is giving you a completely free month of legally binding coverage with no cost attached. Instead, it often refers to one of these setups:

- Your first bill is delayed until a later date.

- Your upfront payment is very small compared to a normal deposit.

- The insurer spreads the opening cost across future monthly installments.

- A promotion or partner financing arrangement temporarily reduces the initial payment.

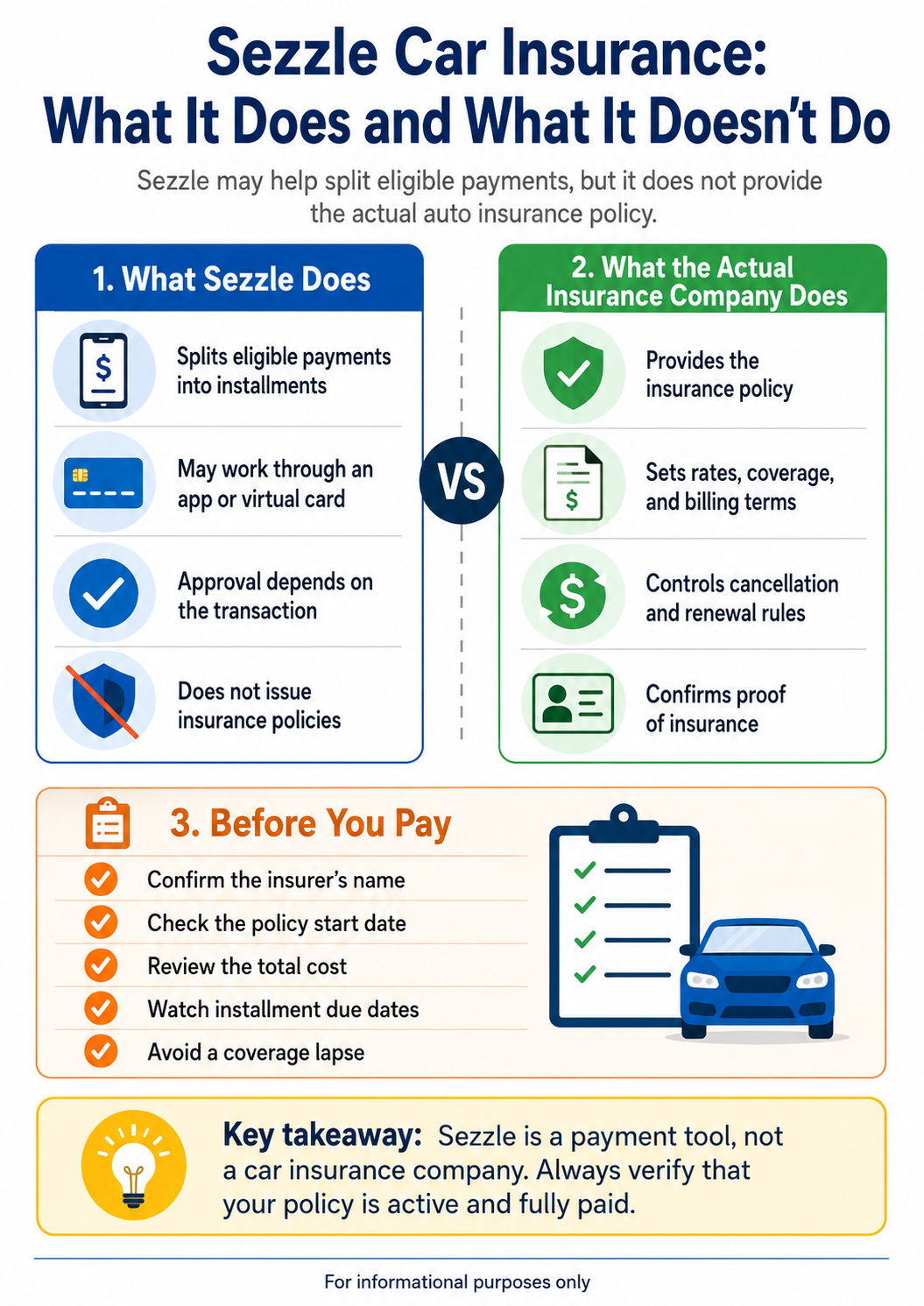

That is why many so-called free-month offers are really part of broader pay later solutions. The policy still has a cost, but the payment timing is adjusted to make coverage easier to start.

Is First Month Free Insurance Legit?

It can be legitimate, but you should read the details carefully. A trustworthy insurer or broker may advertise flexible billing, promotional credits, or low-start plans. The issue is not always fraud. The issue is that the phrase “first month free” can make drivers think the policy has no early cost at all, when the reality is often more complicated.

If you want to understand the fine print behind flexible billing, it also helps to review how pay later car insurance contracts are usually structured.

Why Drivers Search for This Type of Policy

Most people are not searching for first month free auto insurance because they expect a gift from an insurer. They are looking for breathing room. A driver may need insurance immediately after buying a vehicle, renewing registration, switching carriers, or fixing a lapse in coverage. In these moments, reducing the first payment matters more than anything else.

- They need same-day proof of insurance.

- They are between paychecks.

- They just purchased a car and already paid other large expenses.

- They want to avoid a large deposit.

- They are trying to restart coverage after a lapse.

If that sounds familiar, you may also want to compare instant auto insurance with no down payment or instant coverage buy now pay later options.

What to Watch Out For Before You Buy

Any offer built around “free” language deserves extra scrutiny. The goal is not just finding the lowest first bill. The goal is finding a policy you can actually maintain. A plan with almost nothing due today may still become expensive very quickly if fees, financing costs, or higher monthly premiums are built in.

- When exactly the first real payment is due

- Whether any installment or service fees are added

- Whether a missed payment cancels coverage quickly

- Whether the advertised “free” period is actually a credit or just a deferral

- The full premium over the life of the policy

For more on the rules that may shape these offers, see deferred payment car insurance regulation.

Best Alternatives to First Month Free Auto Insurance

If you cannot find a real first month free offer, that does not mean you are out of options. In practice, the following alternatives are often better and easier to qualify for:

How to Improve Your Chances of Finding a Good Offer

You do not always need a special promotion to get a low-start policy. Sometimes the better strategy is improving the quote structure itself. Choosing liability-only coverage, raising deductibles where appropriate, comparing several providers, and checking companies that specialize in flexible payment plans can all reduce what you owe at signup.

- Compare several quotes instead of applying to only one company

- Ask whether billing can be split or delayed

- Start with the minimum coverage you legally need, then review upgrades later

- Check your eligibility for flexible plans at BNPL car insurance eligibility

- Use a side-by-side tool such as compare buy now pay later car insurance

Who Might Benefit Most From This Type of Search?

First month free auto insurance is especially attractive to first-time drivers, people restarting a policy, and anyone handling a sudden vehicle purchase. But the best solution depends on the situation. A first-time driver may benefit more from a beginner-focused flexible plan than from chasing a rare promotional headline.

That is why it may also be worth looking at BNPL car insurance for first-time drivers or reviewing the best pay later companies if you want broader options.

Is No Credit Check the Same Thing as First Month Free?

No. These are separate ideas. A no credit check plan focuses on underwriting or qualification methods. A first month free offer focuses on the payment schedule or marketing angle. Sometimes a driver looking for one may also be interested in the other, but they should not be treated as the same product.

If credit is part of your concern, read more about no credit check pay later car insurance.

Bottom Line: Should You Chase “First Month Free”?

The phrase sounds appealing, but most drivers should focus less on “free” and more on affordable activation. A reliable low-upfront or delayed-payment policy is usually more useful than a flashy offer that hides costs in the next bill. If you compare carefully and read the terms, you can often get nearly the same cash-flow benefit without falling for a misleading headline.

To explore flexible options from a broader angle, you can also visit our home page, review our FAQs, or contact us through the contact page if you want to understand which type of plan may fit your situation best.

Frequently Asked Questions

Can I really get a full month of auto insurance for free?

Usually not in the literal sense. Most offers are delayed billing, reduced upfront payments, or temporary promotional credits rather than a truly free month of coverage.

What is usually better than chasing a “first month free” offer?

For many drivers, low upfront cost plans or no upfront payment options are more realistic and easier to compare.

Can I still get instant coverage while paying later?

Yes. Many providers can activate coverage quickly even when the first full payment is delayed or split into later installments.